Small and medium-sized businesses (SMEs) play a vital role in the UAE’s economy, contributing significantly to innovation, employment, and economic growth. As the UAE continues to strengthen its financial and regulatory framework, businesses of all sizes are expected to comply with Anti-Money Laundering (AML) regulations designed to combat financial crime and protect the integrity of the country’s financial system.

Many SMEs mistakenly believe that AML obligations apply only to banks and large financial institutions. However, a growing number of businesses across various industries are subject to AML requirements, including real estate firms, corporate service providers, accounting firms, legal consultancies, precious metal dealers, and other designated sectors.

Failure to comply with AML regulations can result in financial penalties, reputational damage, regulatory investigations, and business disruptions. For this reason, implementing a robust AML compliance program is no longer optional—it is an essential component of responsible business management.

This guide provides a practical AML compliance UAE consulting checklist for small and medium-sized businesses operating in the UAE and explains how organizations can strengthen their compliance frameworks.

Understanding AML Compliance in the UAE

Anti-Money Laundering (AML) regulations are designed to prevent businesses from being used to facilitate:

- Money laundering

- Terrorist financing

- Fraud

- Financial crimes

- Sanctions violations

- Illicit financial activities

AML regulations require businesses to identify risks, verify customers, monitor transactions, maintain records, and report suspicious activities when necessary.

Many organizations rely on experienced legal consultants in UAE to interpret regulatory obligations and develop compliance programs tailored to their operations.

Why AML Compliance Matters for SMEs

Some small businesses assume that regulators primarily focus on large corporations.

In reality, regulatory authorities expect all covered businesses to maintain effective compliance systems regardless of size.

Strong AML compliance helps SMEs:

- Avoid regulatory penalties

- Protect business reputation

- Strengthen customer trust

- Improve banking relationships

- Reduce financial crime risks

- Support sustainable growth

Organizations that invest in compliance often gain a competitive advantage by demonstrating professionalism and accountability.

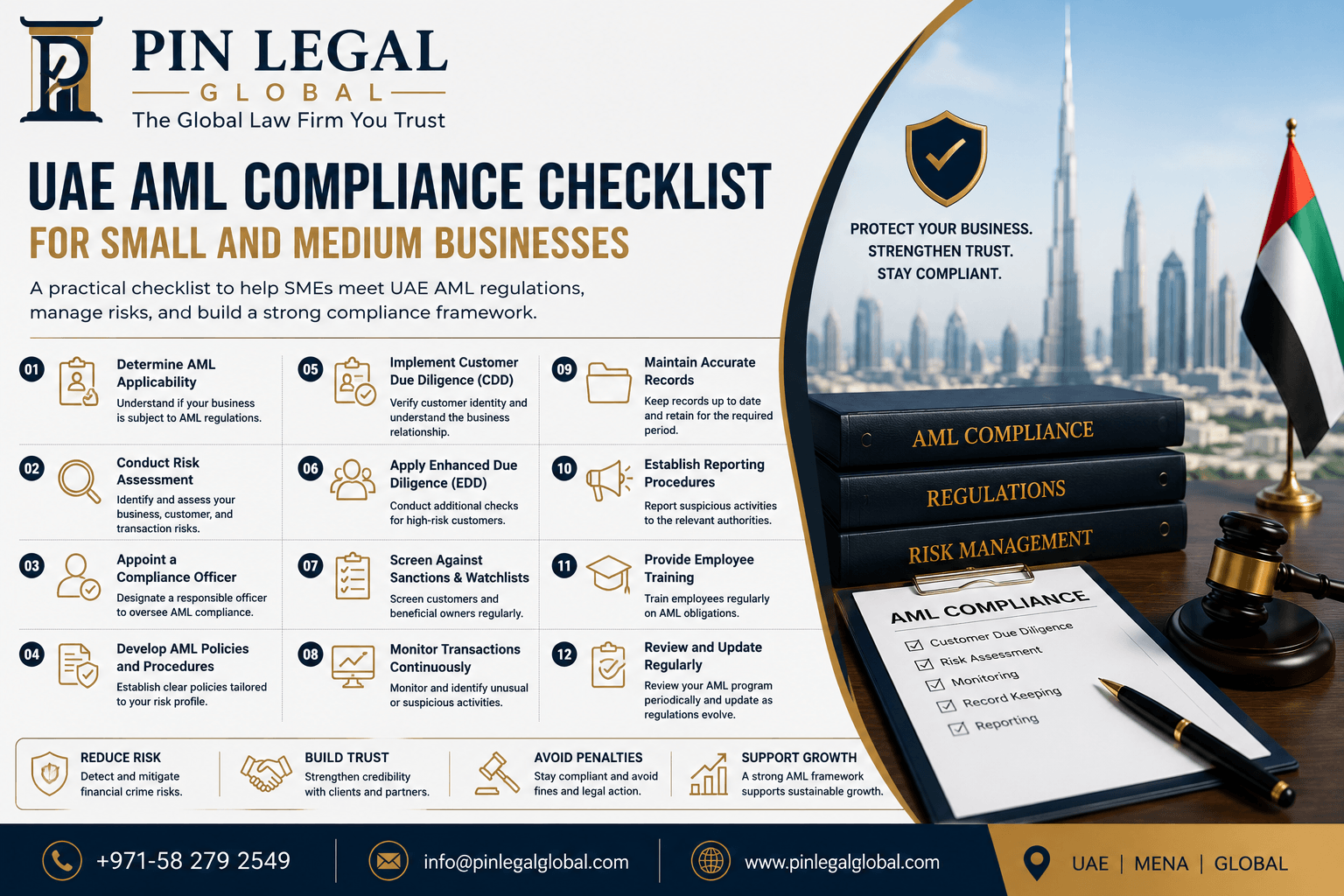

AML Compliance Checklist for UAE SMEs

The following checklist provides a practical framework for businesses seeking to strengthen their AML programs.

1. Determine Whether Your Business Is Subject to AML Regulations

The first step is understanding whether your business falls within a regulated category.

Industries commonly subject to AML requirements include:

- Financial services

- Real estate

- Accounting services

- Auditing firms

- Corporate service providers

- Legal advisory firms

- Precious metal and gemstone dealers

- Trust and company formation providers

Businesses involved in company formation UAE services often face heightened AML obligations due to the nature of their activities.

If uncertainty exists, consulting a UAE compliance advisory firm can help clarify regulatory responsibilities.

2. Conduct a Business-Wide AML Risk Assessment

Risk assessment forms the foundation of an effective compliance program.

Organizations should evaluate:

Customer Risks

Assess the types of clients served and their risk profiles.

Geographic Risks

Identify exposure to high-risk jurisdictions.

Transaction Risks

Review transaction volumes, complexity, and patterns.

Product and Service Risks

Evaluate how specific products or services may be vulnerable to misuse.

Professional AML compliance UAE consulting services often begin with comprehensive risk assessments that help businesses identify and prioritize compliance risks.

3. Appoint a Compliance Officer

Every organization should designate an individual responsible for overseeing AML compliance activities.

Responsibilities may include:

- Monitoring compliance programs

- Managing reporting obligations

- Coordinating employee training

- Conducting internal reviews

- Communicating with regulators

The designated officer should have sufficient authority, knowledge, and resources to fulfill these responsibilities effectively.

4. Develop AML Policies and Procedures

Businesses should establish written policies that clearly define compliance expectations.

Key policy areas include:

- Customer Due Diligence (CDD)

- Enhanced Due Diligence (EDD)

- Risk assessments

- Recordkeeping

- Suspicious activity reporting

- Employee responsibilities

- Internal controls

Well-documented policies help ensure consistency across the organization and support broader corporate compliance UAE objectives.

5. Implement Customer Due Diligence Procedures

Customer Due Diligence (CDD) is one of the most important AML requirements.

Businesses should verify customer identities and understand the nature of business relationships.

CDD procedures should include:

- Identity verification

- Beneficial ownership identification

- Risk classification

- Customer screening

- Ongoing monitoring

Organizations offering business legal services UAE or financial-related services often require enhanced due diligence procedures for higher-risk clients.

6. Conduct Enhanced Due Diligence for High-Risk Customers

Some customers present greater AML risks than others.

Examples may include:

- Politically Exposed Persons (PEPs)

- High-risk jurisdictions

- Complex ownership structures

- Unusual transaction patterns

Enhanced Due Diligence (EDD) may involve:

- Additional verification measures

- Increased monitoring

- Senior management approval

- Enhanced documentation requirements

Legal advisors specializing in regulatory compliance UAE can help businesses establish risk-based EDD frameworks.

7. Screen Customers Against Relevant Lists

Businesses should implement screening procedures that identify potential compliance concerns.

Screening may include:

- Sanctions lists

- Watchlists

- Regulatory databases

- Internal risk databases

Regular screening helps organizations detect risks early and demonstrate proactive compliance efforts.

8. Establish Transaction Monitoring Procedures

Monitoring customer transactions is essential for identifying suspicious activity.

Businesses should monitor for:

- Unusual payment patterns

- Inconsistent transaction behavior

- Structuring activities

- High-value transactions

- Unexplained financial activity

The level of monitoring should reflect the organization’s risk profile and operational activities.

9. Maintain Accurate Records

Recordkeeping is a core AML obligation.

Businesses should maintain documentation relating to:

- Customer identification

- Risk assessments

- Transaction records

- Compliance reviews

- Internal reports

- Employee training

Proper record management supports regulatory reporting requirements and facilitates compliance audits.

Organizations often seek UAE regulatory filing support to strengthen documentation and reporting practices.

10. Create Suspicious Activity Reporting Procedures

Employees should understand how to identify and report suspicious activities.

Reporting procedures should include:

- Internal escalation processes

- Documentation requirements

- Reporting timelines

- Regulatory notification procedures

Clear reporting frameworks improve compliance effectiveness and reduce regulatory risks.

11. Provide AML Training for Employees

Employee awareness is critical to the success of any compliance program.

Training should cover:

- AML regulations

- Customer due diligence

- Suspicious activity indicators

- Reporting obligations

- Internal procedures

Regular training helps employees recognize risks and fulfill compliance responsibilities.

Many organizations incorporate AML education into broader UAE corporate governance advisory initiatives.

12. Conduct Regular Compliance Reviews

AML programs should be reviewed periodically to ensure effectiveness.

Reviews may assess:

- Policy adequacy

- Operational controls

- Training effectiveness

- Risk assessment accuracy

- Reporting procedures

Internal audits and independent assessments help identify gaps and opportunities for improvement.

13. Monitor Regulatory Developments

AML regulations continue to evolve.

Businesses should stay informed regarding:

- New legal requirements

- Regulatory guidance

- Enforcement trends

- Industry-specific developments

Many SMEs rely on professional legal consultants UAE to monitor regulatory changes and provide practical compliance recommendations.

14. Strengthen Corporate Governance

AML compliance should form part of broader governance and risk management strategies.

Strong governance structures help organizations:

- Improve accountability

- Strengthen oversight

- Enhance transparency

- Support compliance objectives

Businesses that integrate AML requirements into governance frameworks are often better positioned to manage regulatory expectations.

Common AML Compliance Mistakes Made by SMEs

Small businesses frequently encounter compliance challenges due to limited resources or lack of expertise.

Common mistakes include:

- Inadequate risk assessments

- Poor customer verification procedures

- Insufficient documentation

- Lack of employee training

- Weak transaction monitoring

- Failure to update policies

- Delayed reporting of suspicious activities

Addressing these issues proactively can significantly reduce compliance risks.

How Legal Advisors Support AML Compliance

AML compliance involves more than completing checklists.

Experienced legal advisors assist businesses with:

- Risk assessments

- Policy development

- Compliance audits

- Employee training

- Regulatory reporting

- Governance frameworks

- Ongoing compliance monitoring

Through corporate legal advisory UAE services, organizations can develop compliance programs that align with both regulatory requirements and business objectives.

Why Businesses Choose Pin Legal Global

Maintaining AML compliance requires a combination of legal expertise, risk management knowledge, and practical implementation strategies.

Pin Legal Global provides comprehensive AML compliance UAE consulting services for SMEs and larger organizations operating across the UAE. The firm assists clients with risk assessments, compliance framework development, policy drafting, governance reviews, and regulatory preparedness.

With experience in regulatory compliance UAE, corporate governance, company formation, and business advisory services, Pin Legal Global helps organizations build strong compliance foundations while supporting long-term growth.

Whether establishing a new compliance program or strengthening existing controls, Pin Legal Global delivers tailored legal solutions designed to address modern regulatory challenges.

Conclusion

AML compliance is no longer a concern reserved for large financial institutions. Small and medium-sized businesses across the UAE face increasing regulatory expectations and must take proactive steps to identify, manage, and mitigate financial crime risks.

By following a structured compliance checklist, implementing effective controls, and seeking support from experienced legal consultants in UAE, businesses can strengthen their compliance posture and reduce regulatory exposure.

A strong AML framework not only helps organizations meet legal obligations but also enhances reputation, improves operational resilience, and supports sustainable growth. Investing in professional AML compliance UAE consulting services can provide SMEs with the guidance and confidence needed to navigate today’s evolving regulatory environment successfully.